- 137

- 792 552

finRGB

India

Приєднався 27 лип 2016

Welcome to the finRGB FRM Exam Prep Channel! This channel is dedicated to helping you excel in the FRM Part 1 and Part 2 exams. For comprehensive study materials (instructional videos, notes, question sets and review videos), please visit our website at www.finRGB.com. While you're here, make sure you subscribe to this channel to stay updated on high-quality videos designed to simplify complex risk management concepts, provide in-depth explanations, and offer practical tips.

Bhuvnesh Khurana, CFA, FRM

(www.linkedin.com/in/bhuvnesh-khurana-cfa-frm-b06142/)

Bhuvnesh Khurana, CFA, FRM

(www.linkedin.com/in/bhuvnesh-khurana-cfa-frm-b06142/)

Credit Valuation Adjustment (CVA) for a European Option | FRM Part 2 (Credit Risk) | Solved Example

In this video from the FRM Part 2 curriculum, we take a look at the concept of Credit Valuation Adjustment (CVA) for the simple, but special case of a European option. We solve a numerical example taken from Reading 12 of Book 2 of the FRM Part 2 curriculum. For more preparation resources related to the FRM Part 2 exam, please visit the course page below:

www.finRGB.com/courses/frm-part-2-online-course

www.finRGB.com/courses/frm-part-2-online-course

Переглядів: 484

Відео

Net Stable Funding Ratio (NSFR) Explained | FRM Part 2 | Liquidity Risk

Переглядів 704Місяць тому

In this video from the FRM Part 2 curriculum, through a simple solved example, we explore the concept of Net Stable Funding Ratio (NSFR), which is defined to be the ratio of available stable funding to required stable funding. For more preparation resources for the FRM Part 2 exam, please browse over to the course page below: www.finRGB.com/courses/frm-part-2-online-course

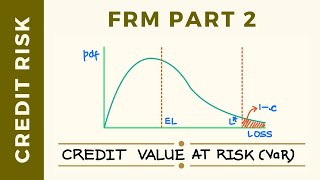

Credit Value-at-Risk (VaR) | FRM Part 2 | Credit Risk

Переглядів 553Місяць тому

In this video from the FRM Part 2 curriculum, we take a look at the measure of Credit Value at Risk (Credit VaR). Credit VaR is the credit risk loss over a certain period that will not be exceeded at the chosen confidence level. For more videos and preparation resources related to FRM Part 2 preparations, please head over to the course page below: www.finRGB.com/courses/frm-part-2-online-course

Positive Definite Correlation Matrices | FRM Part 1 (Quantitative Analysis)

Переглядів 258Місяць тому

In this video from the FRM Part 1 curriculum, we will explore this concept of structured correlation matrices, specifically, this property of the correlation matrix being "Positive Definite". For more videos and preparation resources related to the FRM Part 1 exam, please refer to the course page below: www.finRGB.com/courses/frm-part-1-online-course

Value at Risk (VaR) - Advantages & Disadvantages Explained | FRM Part 1 / FRM Part 2 | CFA Level 2

Переглядів 7782 місяці тому

In this video we will recap the definition of Value-at-Risk (VaR), how it is calculated for a simple loss distribution and simple profit distribution and list down its advantages and disadvantages. For more videos related to FRM Part 1 and FRM Part 2 preparations, please head over to the respective course pages listed below: 1) FRM Part 1: www.finRGB.com/courses/frm-part-1-online-course 2) FRM ...

Expected Value and Variance of a Discrete Random Variable | FRM Part 1 | Quantitative Analysis

Переглядів 3045 місяців тому

In this video from the FRM Part 1 curriculum, we look at the concept of Expected Value and Variance of a discrete random variable. For this purpose, we use a solved example pulled from an old GARP Sample Paper. The learning objectives for this video are as below: A) Understand and apply the concept of a mathematical expectation of a random variable B) Describe the four common population moments...

Index Credit Default Swaps Explained | FRM Part 2 | Credit Risk

Переглядів 1,7 тис.5 місяців тому

In this video, we explore Index Credit Default Swaps (Index CDS) - contracts that allow investors to buy or sell credit protection on multiple names using a single transaction. The video first explores the mechanics of a simple or single name CDS and then provides extensions for an index CDS. For more videos and preparation resources aimed at FRM Part 2 preparations, please see the course page:...

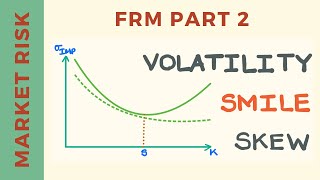

Volatility Smile and Skew | FRM Part 2 | Market Risk

Переглядів 2,4 тис.6 місяців тому

In this video, we explore this concept of volatility smile and skew. This topic comes up in the Market Risk book (Book 1) of the FRM Part 2 curriculum. For more preparation resources related to FRM Part 2 exam, please follow the link below: www.finRGB.com/courses/frm-part-2-online-course

Overnight Index Swaps (OIS) Explained | Mechanics and Use (FRM Part 1)

Переглядів 4,5 тис.6 місяців тому

In this video from the FRM Part 1 curriculum, we explore Overnight Index Swaps (OIS). We take a look at the mechanics of OIS that reference SOFR (Secured Overnight Financing Rate) i.e. how they work and how they can be used in a very practical situation that involves transforming the nature of liabilities of a financial institution from floating to fixed. For more videos and preparation materia...

Study Sequence for FRM Part 2 (2024)

Переглядів 1,7 тис.6 місяців тому

In this video, we take a look at a suggested study sequence for FRM Part 2 (2024) - a sequence that assumes a 16-week preparation period. A more detailed study sequence is given in the link here: www.finRGB.com/frm-part-2-study-plan For FRM Part 2 preparation resources, please browse over to the course page here: www.finRGB.com/courses/frm-part-2-online-course

Equity Swaps Explained: Pricing and Valuation | CFA Level 2

Переглядів 4,3 тис.Рік тому

In this video from the CFA Level 2 curriculum, we explore how to price and value equity swaps. This video deals with equity vs fixed variant of equity swaps, but the logic and approach used in this video can be extended and cross applied for pricing and valuing other variants (equity vs floating and equity vs equity) as well. The learning objective from CFA Level 2 curriculum is given below: *C...

Liquidity Coverage Ratio (LCR) Explained | FRM Part 2 | Liquidity Risk | CFA Level 2

Переглядів 10 тис.Рік тому

In this video, we take a look at the Liquidity Coverage Ratio (LCR), a liquidity focused ratio introduced as part of the Basel III reforms. The Liquidity Coverage Ratio measures the bank's probable reaction to a liquidity crisis lasting 30 days, ensuring that it has sufficient high-quality liquid assets to deal with the crisis. The ratio ensures that cash outflows that could possibly occur in t...

Bootstrapping | Bootstrap Resampling in Statistics | CFA Level 1 | FRM Part 1 | FRM Part 2

Переглядів 5 тис.Рік тому

In this video from the FRM Part 1, FRM Part 2 and CFA Level 1 curricula, we explore this simple yet powerful statistical technique called Bootstrap. This technique can help arrive at the statistical properties (standard error, sampling distribution) of your chosen estimator for a population parameter without resorting to difficult to defend mathematical assumptions and analysis. For instruction...

Non-Deliverable Forwards (NDFs) Explained | CFA Level 3

Переглядів 11 тис.Рік тому

In this video from the CFA Level 3 curriculum, we explore the mechanics of Non-Deliverable Forwards (NDFs). Non-Deliverable Forwards are OTC derivatives contracts that allow foreign investors to take a view on / hedge exposures to currencies that are not physically deliverable and cash settle the difference between an agreed rate and actual price (at maturity), with the settlement happening in ...

Equity Swaps Explained: Mechanics and Variations | FRM Part 1 | CFA Level 2

Переглядів 23 тис.2 роки тому

In this video from the curricula of FRM Part 1 and CFA Level 2, we explore the mechanics of Equity Swaps - their mechanics, structuring / customization and the use cases that they can be put to. This video focuses on the following learning objectives: FRM Part 1: Identify and describe other types of swaps, including commodity, volatility, credit default, and exotic swaps. CFA Level 2: Describe ...

Moving Average (MA) Models | Time Series Analysis | FRM Part 1 | CFA Level 2

Переглядів 1,7 тис.2 роки тому

Moving Average (MA) Models | Time Series Analysis | FRM Part 1 | CFA Level 2

Credit Exposure Metrics (EFV, EE, PFE) for Interest Rate Swap | FRM Part 2

Переглядів 8 тис.2 роки тому

Credit Exposure Metrics (EFV, EE, PFE) for Interest Rate Swap | FRM Part 2

Covered Vs Uncovered Interest Rate Parity | FRM Part 1 | CFA Level 2

Переглядів 18 тис.2 роки тому

Covered Vs Uncovered Interest Rate Parity | FRM Part 1 | CFA Level 2

Variance Swaps Explained | Mechanics & Use | FRM Part 1 | CFA Level 3

Переглядів 6 тис.2 роки тому

Variance Swaps Explained | Mechanics & Use | FRM Part 1 | CFA Level 3

Do I need to be strong at Math to ace the FRM exam? (FRM Part 1, FRM Part 2)

Переглядів 2,3 тис.2 роки тому

Do I need to be strong at Math to ace the FRM exam? (FRM Part 1, FRM Part 2)

Put Call Forward Parity for European Options (FRM Part 1, CFA Level 1)

Переглядів 3,5 тис.2 роки тому

Put Call Forward Parity for European Options (FRM Part 1, CFA Level 1)

Monte Carlo Variance Reduction using Antithetic Variates (FRM Part 1, Quantitative Analysis)

Переглядів 6 тис.2 роки тому

Monte Carlo Variance Reduction using Antithetic Variates (FRM Part 1, Quantitative Analysis)

Wrong Way Risk - An Introduction (FRM Part 1 / FRM Part 2, Book 2, Credit Risk)

Переглядів 6 тис.2 роки тому

Wrong Way Risk - An Introduction (FRM Part 1 / FRM Part 2, Book 2, Credit Risk)

What does the Autocorrelation vs Lag Plot (Correlogram) tell us? (FRM Part 1, Quantitative Analysis)

Переглядів 7 тис.2 роки тому

What does the Autocorrelation vs Lag Plot (Correlogram) tell us? (FRM Part 1, Quantitative Analysis)

Expected Shortfall for Uniform Distribution (Solved Example)(FRM Part 1, Valuation and Risk Models)

Переглядів 3,8 тис.2 роки тому

Expected Shortfall for Uniform Distribution (Solved Example)(FRM Part 1, Valuation and Risk Models)

Structural Vs Reduced Form Models of Credit Risk (CFA Level 2, FRM Part 2, Book 2, Credit Risk)

Переглядів 9 тис.2 роки тому

Structural Vs Reduced Form Models of Credit Risk (CFA Level 2, FRM Part 2, Book 2, Credit Risk)

Formula Review for Book 1 (FRM-Part-1, Book 1, Foundations of Risk Management)

Переглядів 1,2 тис.2 роки тому

Formula Review for Book 1 (FRM-Part-1, Book 1, Foundations of Risk Management)

Vasicek Model Vs Cox Ingersoll Ross (CIR) Model (FRM Part 2, Book 1, Market Risk)

Переглядів 7 тис.3 роки тому

Vasicek Model Vs Cox Ingersoll Ross (CIR) Model (FRM Part 2, Book 1, Market Risk)

May I know for calculating the fair value of swap, why we use 0.64current exchange rate, but not the projected forward rate?

There are two ways you can do this valuation: Method 1 is to find the present value of the respective cash flows in the two currencies separately. Then, you convert the PV of the cash flows in the 'other' currency to the currency in which value is being calculated by using the current exchange rate. This is because the PV of cash flows is as of today. Method 2 is to find the net cash flow on each settlement date using the forward exchange rate as of that date and then discount all netted cash flows to today. Both methods give the same final answer.

what is a ZCV?

ZCB: Zero Coupon Bond

amazing explanation

if we condition on F, where F = 0 , why do we not get back to PD(i)?

PD is the unconditional probability of default. You'll get it if you calculate the expectation (i.e. probability weighted average) of conditional probability of default (conditional on various chosen values of F).

@finRGB , So the notional value won't change as the FX rates are locked in at the beginning and since EUR/USD has their own interest rate (Interest rate parity). Won't it have two risk: 1) Interest rate fluctuation risk 2) FX currency risk (where proceeds are received in quote currency and to covert the the same in base currency?

Amazing explanation! thank you so much, it was really helpful

Glad that the video was helpful, Jaqueline.

Isn't the left tail is for the loss distribution and right tail for the profit distribution?

Extremely clear, as usual ... which is key for a video on such a technical topic.

Very clear indeed! Thanks!

Glad you found the video helpful, Fabio.

If we use 3 year historical data, will it predict loss for the next 3 years?

Thanks a lot for the best explain and derivation of the BM! May I ask where is the 2nd part of this topic? That how you convert back from discrete to continuous. Really appreciate it!

Thanks Sir, Simplest explanation😃

Sir an example would be really helpful to grasp the concept better..

The aim was to present the concept in its most general sense (without resorting to any approach or technique to calculate Credit VaR). Will surely add a solved example in a video on CreditMetrics / Vasicek models.

Great video as usual ! Thank you so much for clarifying this concept.

Hey I'm extremely weak in Quants, what should I learn before I take the FRM ? Im planning to write it next year in 2025.

Hello Faisal. Kindly send your queries to finRGB@gmail.com.

Thank you for the video

indians are everywhere now. I started from programming tutorials and now i watch a finance tutorial and look at this :O

very well explained

Great video as always ! I just have a quick question, what's the difference between the usual VaR and Credit VaR ?

Thank you for the appreciation, Haythem. Will do a short video on Credit VaR.

@@finRGB Thank you so much, can't wait to see it !

Expected Shortfall fixes some of the disadvantages that VaR has. VaR says how much loss can be expected at a certain likelihood. E.S. tells you more about the shape of the bell curve and what happens beyond the VaR level.

Great insight.

Wow

Does this include Machine learning?

You can find the updated version of the study plan here: www.finRGB.com/frm-part-1-study-plan (includes the machine learning readings).

Very helpful video. Thank you. On the Volatility smile graph (for bullish markets), I guess the video does not explain on why the In-the-money calls have an Implied Vol (IV) that is so much higher than the At-the-money calls. Would you be able to explain briefly, please?

If market have the sentiment that stock will go down in futre, investors will sell ITM calls to earn much elevated premium and hence demand of such ITM calls increases.

Thanks a lot sir..... :)

Question: What is the diffrence between the calculation the economic capital and the IRB Risk weight function ? and btw your one of the best teacher i've encontered in youtube thank so much for your videos !

A firm calculates economic capital to size up its buffers meant to absorb losses owing to various risk types (market, operational, credit etc.). It's an internal calculation aimed to have enough capital to limit the probability of financial distress (this probability can be picked based on the firm's target credit rating). Internal Ratings Based (IRB) approach is meant to calculate RWA that are specific to credit risk. It comes as part of Basel II / Basel III, for calculation of regulatory capital.

Nice explanation

thank you!!!

Very well explained can you also try to make some videos on option Greeks, Black-Scholes model

Thank you for the appreciation, Joseph. Yes sure, will do.

For Case B, if 3m implied SOFR is 1.70%, wouldn’t I make a loss on the futures instead of a gain? And the loss from futures will add on to the overall borrowing cost?

For Case B, the 3m implied SOFR will be 100 - 98.70 = 1.30(%). This will imply a gain / loss on futures position equal to 100 * (98.495 - 98.70) * 25 * 100 = -51,250 (i.e. loss, since it is negative). In this Case B, borrowing cost is 100mn * (1.30% + 2%) * 0.25 = 825,000. Adding the borrowing cost and loss gives the total cost to be 876,250 i.e. same as Case A.

Tks!!

I just realised this is the only educational video on IRP, so perfect and making the learner's life easy😃

Thank you for the appreciation, Annu.

Very well explained

Intuitive way of understanding why the law of large numbers is talking about mean, and there is nothing that stops us from fluctuating a lot

Superb explanation.

Thank you for the appreciation, @afia_begum_chowdhury

Great presentation, thank you sir, but can you tell me why u divided by 10,000 to get the fwd rate?

This is because forward exchange rates are quoted in points over and above the spot exchange rate. Before adjusting the spot, you need to divide the quoted amount by 10,000.

Question : what's the diffrence between vasicek for credit risk capital and this vasicek ? Btw your the only one who explain's advanced concepts with simple words in youtube thank you so much.

Thank you for the appreciation. This Vasicek model is an interest rate model i.e. provides a possible means of evolution of the "short rate" over time. The Vasicek model for credit risk capital makes use of the Gaussian copula and one factor model to arrive at the loss distribution for a portfolio of loans / credits. From the loss distribution, an extreme loss can be read and credit risk capital computed. The video for this model is available here: ua-cam.com/video/t9OOTbyOWhs/v-deo.htmlfeature=shared

Hi does anyone trade 3msofr futures?

Very good and succint explanation. Do you do a case example on those calculations anywhere on your channel? it would be really great if you go through the steps with examples.

Thank you for the kind words, Prof. Hassan. At the moment, no, but will cater to this in one of the future videos.

This video forms Part 2 of three videos on Binomial Option Pricing Model. The other parts are available here: Part 1 (Perfect Hedge approach): ua-cam.com/video/GCamKDy9p2M/v-deo.html Part 2 (Replicating Portfolio approach): ua-cam.com/video/Ld9E4f5xxK0/v-deo.html

This video forms Part 2 of three videos on Binomial Option Pricing Model. The other parts are available here: Part 1 (Perfect Hedge approach): ua-cam.com/video/GCamKDy9p2M/v-deo.html Part 3 (Risk Neutral approach): ua-cam.com/video/fEu-2uS7534/v-deo.html

I like the way you presenting the concept! Simple and clear! Cheers!

Thank you for the appreciation, @saikitng15

P0= around 150?

Correct. 137.30 + PV(13.5)

answer ?

What if my null is U> 10,Alt is U<10 and calculated CI came U<15. Then U>15 will be inconsistent with CI. But not 10< U<15. What does this mean?

Wow that was superb. Thank you so much.

Thanks for the info @finRGB! Can I clarify if the margin on the swap is different from that fix payable leg paid to the bank by the hedge fund? or is it the same thing

goated video thanks bro

Thank you for the appreciation, Fraser.

the explanation is incorrect. In fact the difference between the "risk neutral world" and the "real world" doesn't affect the volatility of the stochastic process but only its drift term (mean).

That's what the assumptions underpinning the Black Scholes assert. Realized volatility, which is estimated using actual real world fluctuations in asset prices, is associated with a real world perspective. Implied volatility has a risk neutral perspective associated with it. The two can be different if traders feel that implied volatility quotes require an adjustment over and above the expected realized volatility / volatility is stochastic and requires a risk premium / Black Scholes assumptions are violated in practice.

This is the most easy to understand explanation i have ever heard! Thank you so much!

Glad you found the video helpful, @demoiido7655.

Where is the 2% comimg from

It is the fixed spread (200 bps) on top of 3-month SOFR that we are assuming in our simple example.